The most common approach for maintaining a company’s financial transaction records has historically been a manual accounting system. Traditionally, the bookkeeper would physically write a summary of transactions and the final accounts while also maintaining books of accounts, including the cash book, diary, and ledger. The advent of various devices capable of carrying out a variety of accounting tasks was made possible by technical advancements.

A common billing machine, for instance, was created to typewrite a description of the transaction along with the names and addresses of the clients. This device had the ability to compute discounts, add the net total, and publish the necessary information to the necessary accounts. Once the operator had input the necessary data, the customer’s bill was created automatically. These devices integrated functionality from several calculators and typewriters.

The technology improved as a result of the significant rise in transactions. Newer iterations of those machines emerged with the exponential expansion in speed, storage, and processing capacity. They were connected to a computer that ran these devices. Resources must be optimised, decisions made quickly, and control exercised to ensure the success of a growing organisation with the complexity of transactions handled.

As a result, real-time (or spontaneous) data maintenance became practically necessary. With the advent of computerised accounting, this method of preserving accounting records became practical.

Features of Computerised Accounting

Computerised accounting is implemented using accounting software. The foundation of computer accounting is the idea of databases. The idea of creating and keeping diaries, ledgers, and other records, which are necessary when dealing with manual accounting, is eliminated. The following aspects of computerised accounting are often available:

- Online accounting data entry and archiving.

- Purchase and sales invoice prints.

- A logical system for codifying transactions and accounts.

- Every transaction and account is given a special code.

- The grouping of accounts is finished right away.

- Immediate management reports, such as aging statements, stock balances, trading and profit and loss records, stock valuations, GST, return records, payroll reports, etc.

Decisions and Information:

Every organisation functions as a system that absorbs inputs and converts them into outputs. All organisational systems allocate resources in order to achieve certain goals, which is done through the management decision-making process. Information makes resource allocation decisions easier to make, which helps an organisation achieve its goals.

Information is therefore the most crucial organisational resource. Every medium-sized to big company has a solid data system in place that is designed to produce the data needed for decision-making.

Transaction Processing Technologies (TPS) have started to become increasingly important in supporting corporate operations as a result of the growing usage of information systems in organisations. There are three parts to any transaction processing system: input, processing, and output. The input to the IT-based data system must be correct, comprehensive, and authorised since information technology (IT) adheres to the GIGO principle (Garbage in, Garbage out). Automation of the input is used to accomplish this. There are now many tools available to automate a TPS’s input procedure.

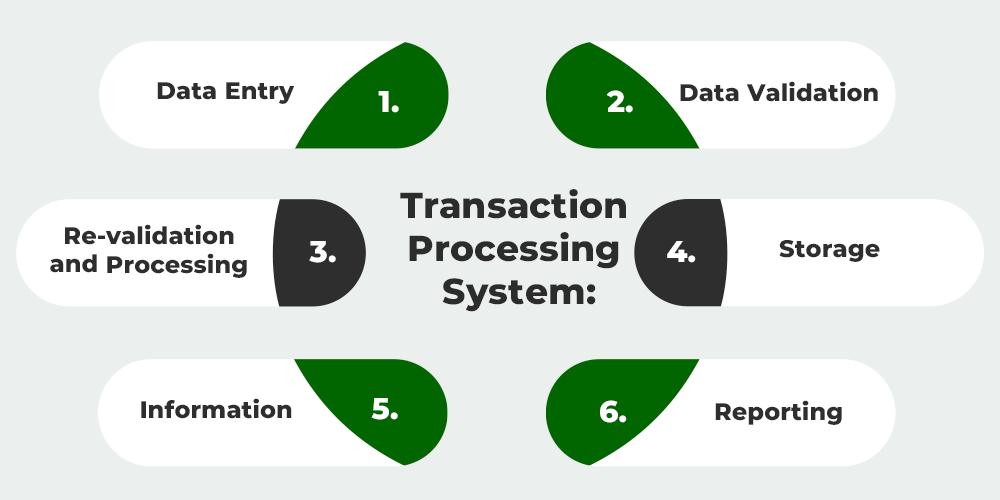

Transaction Processing System:

One of the earliest computerised systems to serve the needs of major corporate operations is the transaction processing system (TPS). The goal of a typical TPS is to capture, process, validate, and store transactions that take place across a business’s numerous functional areas for later retrieval and use. An exchange may be internal or external. A department is said to have engaged in an interior transaction when it requests material supplies from retailers.

However, an external transaction occurs when the buying department buys supplies from a supplier. Financial accounting solely includes external transactions in its purview.

Financial accounting solely includes external transactions in its purview. The following stages are included in TPS while processing a transaction:

i. Data Entry:

Prior to processing, the action data must be entered into the system. To enter data, a number of input devices are available, including a keyboard and mouse.

ii. Data Validation:

By comparing an equivalent with certain established criteria or known facts, it verifies the input file’s correctness and dependability. Procedures for mistake identification and rectification carry out this validation. The control mechanism, which compares the quality of the input with the actual input is intended to identify problems, while error-correction algorithms offer recommendations for providing accurate data input.

iii. Re-validation and Processing:

When valid data representing user actions is met, the processing of knowledge reflecting the actions of the user happens very instantly, much like in the case of the online Transaction Processing (OLTP) system. This is to check the input validity. This process is known as an output validity check.

iv. Storage:

The above-mentioned processed operations result in financial transaction data that, when placed in the transaction database of the computerised system, represent a specific transaction. This suggests that the database contains only transactions that are legitimate.

v. Information:

To provide the required information, the stored data is processed using the query facility. Structured command language (SQL) support is a given for every database supported by a database management system (DBMS).

vi. Reporting:

Finally, reports may be created depending on the necessary information content and according to how beneficial they will be in making decisions.

A straightforward computerised accounting system collects all transaction data as input, stores it on memory media (like a hard drive), and then retrieves it for processing as and when necessary to provide an accounting report as output. The method by which accounting software converts data into information is depicted in the input-process-output diagram below. Execution or real-time operation are both used to process knowledge.

Batch processing is used for massive amounts of offline data that are gathered from several branches or departments. To produce the required reports that are in line with the decision-making need, the full accumulated data set is processed in rounds.

With real-time processing, there is no delay between the transaction and its processing, and the online result is provided in the form of information and reports. The command language known as Structured Query Language produces the accounting reports (SQL). The user can access information that can be set out in a pre-designed accounting report that is pertinent to reports.

Share your thoughts in the comments

Please Login to comment...