Blockchain – Into the Future

Last Updated :

26 Apr, 2022

Accounting, transactions, contracts, and records play a pivotal and defining role in our societal system. They protect assets, and organizational boundaries and uphold the promises between institutions, governments, and corporations. Despite their importance, these have failed to digitize in ways other sectors have. Blockchain technology offers a solution to this. But the touted revolutionary technology is much more than just this and we are yet to realize its limitless potential.

Basics of Blockchain

The advent of blockchain tech brought about a drastic change in several fields of computer science and its applications, arguably, molded the way we live now and such changes occurred in the short span of a decade. Blockchain is the brainchild of an unknown John Doe, introduced in a paper in October 2008 under the name Satoshi Nakamoto. The blockchain technology developed by Nakamoto was not entirely a discovery but a unique method that synchronized three fundamentally different fields, namely Distributed Networks, Cryptography, and Network Servicing protocols. Blockchains, formerly known as blockchains, are distributed ledgers managed by a peer-to-peer network collectively adhering to certain protocols for communication between nodes. Blockchains are highly secure and are often employed in the transaction of digital assets.

Blockchain Mechanism for Noobs

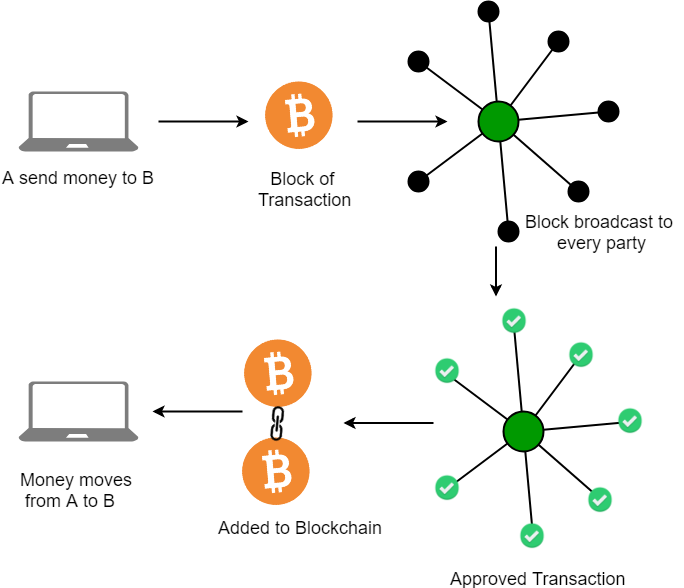

The credibility and uniqueness of this technology are generated from its transaction mechanism. In the transaction, each party has a set of two cryptographic keys one public and one private. The combination of these generates a unique digital signature that provides validation and strong ownership to the parties in the transaction. However, for the transaction to be valid and to prevent fraud, it must be observed and validated by a third party. This is where a distributed network is implemented. The transaction is authorized when a majority of users in the network come to a consensus that it has occurred at the said time. The robustness of a blockchain is generated by the vast number of the network’s users. Cryptocurrencies like bitcoin, litecoin are secure and widely used because they possess a huge network of users, and have amassed large computing power. Bitcoin is secured by 3, 500, 000 TH/s which is greater than the combined hash power of the world’s largest 10, 000 banks. Cryptocurrencies attract a large number of users by providing rewards to certain computers that offer their computing power to the network. Blockchains use a decentralized approach for their protocols. The transaction data is sent to all the nodes that independently come up with a mathematical proof, which is analogous to an image of a physical event. The data is converted into a block and added to the chain if a majority of nodes come to the same conclusion, eliminating the need for a central validating authority. The variables and methodology of the addition of blocks can be altered and vary for different blockchain-based technologies and derivatives.

Philosophical Arguments against Blockchain

The rapid development of a field uncovers many of its flaws and blockchains are no exception to this. Blockchain networks have environmental costs. The encryption and mathematical proofs require great computing power and thus have CO2 emissions which are off the charts. Bitcoin claimed that the energy consumption to keep its network running was more than that of 159 countries. The complexity of Blockchain technology makes it difficult for an ordinary man to understand its many wondrous uses and appreciate it. Cryptocurrencies emerged after the global crisis of 2008 when financial middlemen like banks lost their credibility. However, they now provide satisfactory services in clearing payments and fraud prevention. This has tipped the global scale against the use of blockchain tech in financial sectors. But this can change if certain global events occur, however the stability of the current financial institutions does not indicate any such crisis in the next few years. Network and transaction fees are also considered an underlying issue of blockchain technology. Bitcoin charges 20 cents per transaction while the charges for an end-user in a financial institution such as a bank are very limited. Will society opt to rebuild its entire financial structure from the ground up using a technology it doesn’t completely understand when a robust time-tested financial structure already exists?

Technical Performance Flaws

In a blockchain, as the name implies, the data is added to the ledger as blocks, each with its unique digital signature and timestamp, connected to the previous block. The data stored in each block is potentially unalterable unless the previous is changed which requires permission from a majority of the users. This is the biggest flaw of any blockchain network and is termed as the “51% attack” by Satoshi Nakamoto. If the majority of users agree to something then it can be implemented in a blockchain network making it prone to cyber-attacks. To counter these, blockchain networks are open, i.e any computer can be a node in the network and each network has an insane number of nodes, destroying any potential 51% attack.

The encrypted distributed nature of blockchain makes it very slow, and overly dependent on the computing power of the network. Bitcoin transactions can sometimes take up to several hours to complete. Even the fastest blockchain networks a couple of years back could only complete a few transactions in a second. The best solution to this is the implementation of a Next-Gen High-Throughput Platform. Zilliqa is the most prominent in the long line of companies that are adopting this method to optimize their blockchain networks. The transaction throughput increases with an increase in the size of the network and inbuilt sharding improves and puts Zilliqa in the same league as Mastercard and Visa. Zilliqa can process hundreds and thousands of transactions in a second. Several other solutions to this include platforms like Ethereum and Aerum and technologies such as DAG (Directed Acyclic Graphs).

Prospects

Blockchain technology is relatively new and has not been encompassed in the mainstream industrial sectors. This has resulted in it being neglected for the time being but there has been rapid development in the sector last year. This has displayed several plausible applications in various fields which are not implemented as the pros of this do not outweigh the pros of the existing models. Will the rapid development of Blockchain Technology and increasing ease of its usage be a tipping point in the technological Industrial Revolution 4.0?

Share your thoughts in the comments

Please Login to comment...