Introduction to Blockchain technology | Set 1

Last Updated :

29 Aug, 2023

Blockchain could be a data structure that could be a growing list of information blocks. The knowledge blocks area unit coupled along, such recent blocks can’t be removed or altered. Blockchain is the backbone Technology of the Digital CryptoCurrency BitCoin.

What is Blockchain?

The blockchain is a distributed database of records of all transactions or digital events that have been executed and shared among participating parties. Each transaction is verified by the majority of participants of the system.

It contains every single record of each transaction. Bitcoin is the most popular cryptocurrency an example of the blockchain. Blockchain Technology first came to light when a person or group of individuals name ‘Satoshi Nakamoto’ published a white paper on “BitCoin: A peer-to-peer electronic cash system” in 2008.

Blockchain Technology Records Transaction in Digital Ledger which is distributed over the Network thus making it incorruptible. Anything of value like Land Assets, Cars, etc. can be recorded on Blockchain as a Transaction.

How does Blockchain Technology Work?

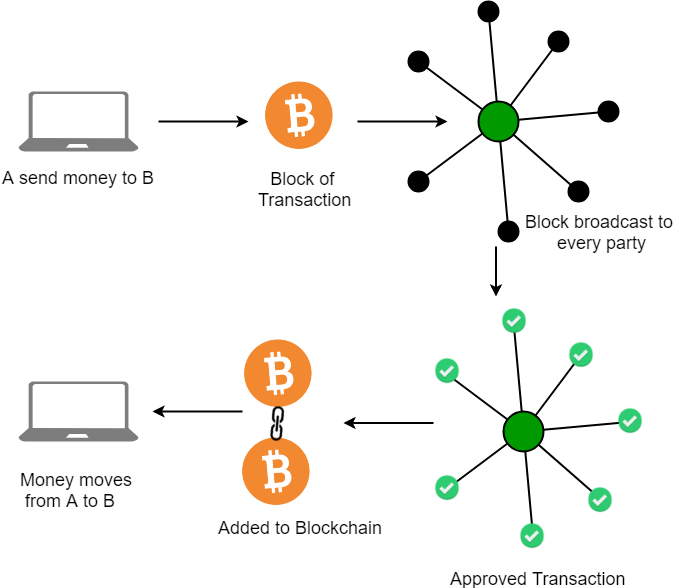

One of the famous use of Blockchain is Bitcoin. Bitcoin is a cryptocurrency and is used to exchange digital assets online. Bitcoin uses cryptographic proof instead of third-party trust for two parties to execute transactions over the Internet. Each transaction protects through a digital signature.

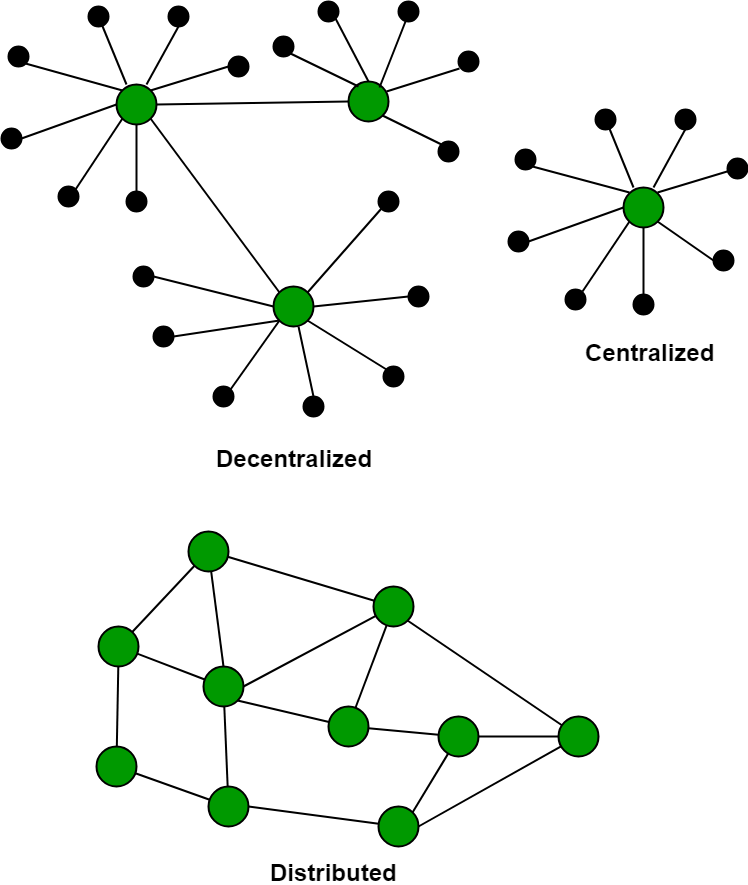

Blockchain Decentralization

There is no Central Server or System which keeps the data of the Blockchain. The data is distributed over Millions of Computers around the world which are connected to the Blockchain. This system allows the Notarization of Data as it is present on every Node and is publicly verifiable.

Blockchain nodes

A node is a computer connected to the Blockchain Network. Node gets connected with Blockchain using the client. The client helps in validating and propagating transactions onto the Blockchain. When a computer connects to the Blockchain, a copy of the Blockchain data gets downloaded into the system and the node comes in sync with the latest block of data on Blockchain. The Node connected to the Blockchain which helps in the execution of a Transaction in return for an incentive is called Miners.

Disadvantages of the current transaction system:

- Cash can only be used in low-amount transactions locally.

- The huge waiting time in the processing of transactions.

- The need for a third party for verification and execution of Transactions makes the process complex.

- If the Central Server like Banks is compromised, the whole system is affected including the participants.

- Organizations doing validation charge high process thus making the process expensive.

Building trust with Blockchain: Blockchain enhances trust across a business network. It’s not that you can’t trust those who you conduct business with it’s that you don’t need to when operating on a Blockchain network. Blockchain builds trust through the following five attributes:

- Distributed: The distributed ledger is shared and updated with every incoming transaction among the nodes connected to the Blockchain. All this is done in real time as there is no central server controlling the data.

- Secure: There is no unauthorized access to Blockchain made possible through Permissions and Cryptography.

- Transparent: Because every node or participant in Blockchain has a copy of the Blockchain data, they have access to all transaction data. They themselves can verify the identities without the need for mediators.

- Consensus-based: All relevant network participants must agree that a transaction is valid. This is achieved through the use of consensus algorithms.

- Flexible: Smart Contracts which are executed based on certain conditions can be written into the platform. Blockchain Networks can evolve in pace with business processes.

What are the benefits of Blockchain?

- Time-saving: No central Authority verification is needed for settlements making the process faster and cheaper.

- Cost-saving: A Blockchain network reduces expenses in several ways. No need for third-party verification. Participants can share assets directly. Intermediaries are reduced. Transaction efforts are minimized as every participant has a copy of the shared ledger.

- Tighter security: No one can tamper with Blockchain Data as it is shared among millions of Participants. The system is safe against cybercrimes and Fraud.

- Collaboration: It permits every party to interact directly with one another while not requiring third-party negotiation.

- Reliability: Blockchain certifies and verifies the identities of every interested party. This removes double records, reducing rates and accelerating transactions.

Application of Blockchain

- Leading Investment Banking Companies like Credit Suisse, JP Morgan Chase, Goldman Sachs, and Citigroup have invested in Blockchain and are experimenting to improve the banking experience and secure it.

- Following the Banking Sector, the Accountants are following the same path. Accountancy involves extensive data, including financial statements spreadsheets containing lots of personal and institutional data. Therefore, accounting can be layered with blockchain to easily track confidential and sensitive data and reduce human error and fraud. Industry Experts from Deloitte, PwC, KPMG, and EY are proficiently working and using blockchain-based software.

- Booking a Flight requires sensitive data ranging from the passenger’s name, credit card numbers, immigration details, identification, destinations, and sometimes even accommodation and travel information. So sensitive data can be secured using blockchain technology. Russian Airlines are working towards the same.

- Various industries, including hotel services, pay a significant amount ranging from 18-22% of their revenue to third-party agencies. Using blockchain, the involvement of the middleman is cut short and allows interaction directly with the consumer ensuring benefits to both parties. Winding Tree works extensively with Lufthansa, AirFrance, AirCanada, and Etihad Airways to cut short third-party operators charging high fees.

- Barclays uses Blockchain to streamline the Know Your Customer (KYC) and Fund Transfer processes while filling patents against these features.

- Visauses Blockchain to deal with business-to-business payment services.

- Unilever uses Blockchain to track all their transactions in the supply chain and maintain the product’s quality at every stage of the process.

- Walmart has been using Blockchain Technology for quite some time to keep track of their food items coming right from farmers to the customer. They let the customer check the product’s history right from its origin.

- DHL and Accenture work together to track the origin of medicine until it reaches the consumer.

- Pfizer, an industry leader, has developed a blockchain system to keep track of and manage the inventory of medicines.

- The government of Dubai looking forward to making Dubai the first-ever city to rely on entirely and work using blockchain, even in their government office.

- Along with the above organizations, leading tech companies like Google, Microsoft, Amazon, IBM, Facebook, TCS, Oracle, Samsung, NVIDIA, Accenture, and PayPal, are working on Blockchain extensively.

Is Blockchain Secure?

Nowadays, as the blockchain industry is increasing day by day, a question arises is Blockchain safe? or how safe is blockchain? As we know after a block has been added to the end of the blockchain, previous blocks cannot be changed. If a change in data is tried to be made then it keeps on changing the Hash blocks, but with this change, there will be a rejection as there are no similarities with the previous block.

Just imagine there is a who hacker runs a node on a blockchain network, he wants to alter a blockchain and steal cryptocurrency from everyone else. With a change in the copy, they would have to convince the other nodes that their copy was valid.

They would need to control a majority of the network to do this and insert it at just the right moment. This is known as a 51% attack because you need to control more than 50% of the network to attempt it.

Timing would be everything in this type of attack—by the time the hacker takes any action, the network is likely to have moved past the blocks they were trying to alter.

Blockchain project ideas

Here are a few project ideas for beginners looking to learn more about blockchain technology:

- Cryptocurrency Wallet: Create a simple cryptocurrency wallet application that allows users to send and receive digital assets.

- Blockchain Explorer: Develop a web-based application that allows users to view and search the transactions on a specific blockchain.

- Smart Contract: Implement a simple smart contract on the Ethereum blockchain that can be used to manage a digital token or asset.

- Voting System: Create a blockchain-based voting system that allows for secure and transparent voting while maintaining voter anonymity.

- Supply Chain Management: Develop a blockchain-based system for tracking the movement of goods and services through a supply chain, providing greater transparency and traceability.

- Decentralized marketplace: Create a decentralized marketplace using blockchain technology where the goods and services can be directly bought by the customers without any intermediary.

- Identity Management: Create a decentralized digital identity management system that allows users to control their personal information and share it securely with others.

These are just a few examples, there are many other possibilities to explore within Blockchain technology.

Future Scope of Blockchain Technology

Finance, supply chain management, and the Internet of Things are just a few of the sectors that blockchain technology has the power to upend (IoT). The following are some potential uses for blockchain in the future:

- Digital Identity: Blockchain-based digital IDs might be used to store personal data safely and securely as well as offer a means of establishing identity without the need for a central authority.

- Smart Contracts: A variety of legal and financial transactions could be automated using smart contracts, self-executing contracts with the terms of the agreement put straight into lines of code.

- Decentralized Finance (DeFi): Using blockchain technology, decentralized financial systems might be built that support peer-to-peer transactions and do away with conventional intermediaries like banks.

- Supply Chain Management: Blockchain technology can be applied to a permanent record of how goods and services have been moved, enabling improved openness and traceability across the whole supply chain.

-Internet of Things (IoT): Blockchain technology may be used to build decentralized, secure networks for IoT devices, enabling them to exchange data and communicate with one another in an anonymous, safe manner.

In general, blockchain technology is still in its early stages and has a wide range of potential applications.

Advantages of Blockchain Technology:

- Decentralization: The decentralized nature of blockchain technology eliminates the need for intermediaries, reducing costs and increasing transparency.

- Security: Transactions on a blockchain are secured through cryptography, making them virtually immune to hacking and fraud.

- Transparency: Blockchain technology allows all parties in a transaction to have access to the same information, increasing transparency and reducing the potential for disputes.

- Efficiency: Transactions on a blockchain can be processed quickly and efficiently, reducing the time and cost associated with traditional transactions.

- Trust: The transparent and secure nature of blockchain technology can help to build trust between parties in a transaction.

Disadvantages of Blockchain Technology:

- Scalability: The decentralized nature of blockchain technology can make it difficult to scale for large-scale applications.

- Energy Consumption: The process of mining blockchain transactions requires significant amounts of computing power, which can lead to high energy consumption and environmental concerns.

- Adoption: While the potential applications of blockchain technology are vast, adoption has been slow due to the technical complexity and lack of understanding of the technology.

- Regulation: The regulatory framework around blockchain technology is still in its early stages, which can create uncertainty for businesses and investors.

- Lack of Standards: The lack of standardized protocols and technologies can make it difficult for businesses to integrate blockchain technology into their existing systems.

- Overall, the advantages of blockchain technology are significant and have the potential to revolutionize many industries. However, there are also several challenges and disadvantages that must be addressed before the technology can reach its full potential.

Share your thoughts in the comments

Please Login to comment...