What Is Project Accounting? and its Principles and Method?

Last Updated :

28 Mar, 2024

Project accounting is a crucial aspect of financial management that focuses on tracking and managing the costs and revenues associated with specific projects or initiatives. project accounting in Project Management is like keeping a separate piggy bank for each project your company works on. It helps you keep track of how much money you’re spending and earning on each project. This way, you can see if you’re making a profit or if you need to adjust your plans to stay on track. It’s especially important for businesses that handle lots of different projects, like construction companies or consulting firms.

Let’s learn about the term “project accounting” in detail.

What Is Project Accounting?

The practice of tracking and managing the costs, revenues, and outlays related to particular projects or endeavors is known as project accounting. Organizations can allocate resources sensibly and make well-informed decisions by using the information it provides about the financial performance of projects.

Project accounting is similar to keeping track of the finances for every project a company works on. It means knowing how much money was made overall and how much was spent (on supplies or labor, for example). This helps the business to make prudent financial decisions and guarantees that all projects stay within budget.

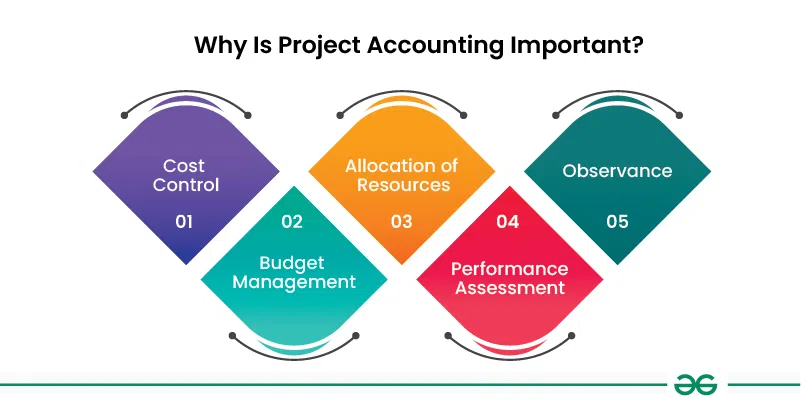

Why Is Project Accounting Important?

Project accounting is essential for several reasons:

Why Is Project Accounting Important

- Cost Control: It is similar to keeping an eye on your expenses. By using project accounting to track your project’s expenses, you can find areas where you can cut costs or use less resources.

- Budget Management: You can make sure that your expenses are within your budget by using project accounting. By keeping track of your expenditures and comparing them to your budget, it helps you stick to your financial plan.

- Allocation of Resources: Think about making sure you are using your resources wisely. Project accounting allows you to monitor the utilization of your resources, including personnel and supplies. This helps you allocate resources as efficiently as possible to finish the current task.

- Performance Assessment: Project accounting can assist you in evaluating your project’s financial performance. By figuring out whether you’re profitable or not, you can make adjustments by figuring out what is and is not working.

- Observance: Project accounting ensures that your project complies with all applicable accounting rules and regulations. This avoids any financial difficulties or issues with regulators by keeping everything in order and in compliance with the law.

How Does Project Accounting Work?

Project accounting involves several key steps:

- Budgeting: This entails determining your project’s financial strategy. You project how much money you’ll need for overhead, labor, supplies, and equipment, among other expenses. By creating a budget, you can make sure you have enough money to finish the project successfully and can allocate resources more effectively.

- Cost tracking: As soon as your project starts, you keep a close eye on every penny you spend. This involves keeping track of all payments made, be they for supplies, subcontractors, salaries, or other expenses. Keeping track of your expenses in real time can help you stick to your spending plan.

- Revenue Recognition: You recognize revenue as your project moves forward in accordance with predetermined completion stages or milestones. For instance, in a building project, revenue might be recorded upon the completion of specific stages such as the framing or foundation laying. In order to appropriately portray the project’s financial performance, this step is essential.

- Reporting: In order to shed light on the project’s financial situation, reporting entails compiling and evaluating financial data. Reports usually contain data on actual costs, revenue, profitability, and variances from the budget. Stakeholders can use these reports to make educated decisions by understanding the project’s financial situation.

- Analysis: To find trends, patterns, and possible hazards, you delve further into the financial data in this step. You could examine elements like revenue delays, cost overruns, or unforeseen costs. You can enhance financial management procedures, allocate resources optimally, and proactively handle problems by carrying out in-depth analysis.

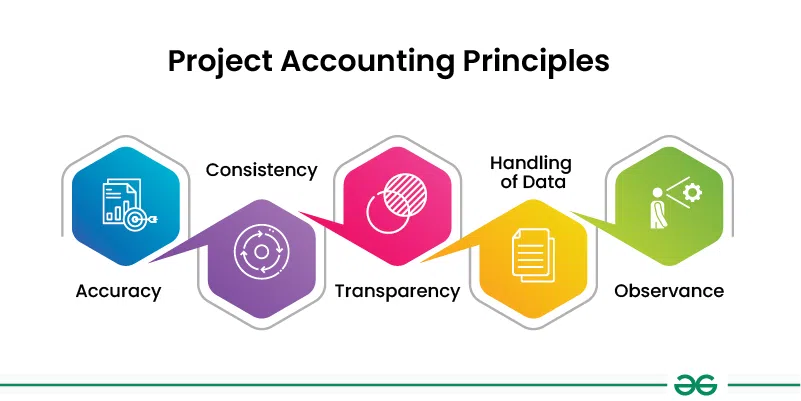

Project Accounting Principles

Key principles of project accounting include:

Project Accounting Principles

- Accuracy: The primary goal of project accounting is to ensure that the figures accurately reflect the amount of money earned and spent on each project.

- Consistency: Consider consistency as applying the same set of rules to every game you play. All projects in project accounting adhere to the same accounting policies and procedures. This guarantees fairness and facilitates the comparison of financial data.

- Transparency: Transparency is a goal of project accounting, giving stakeholders quick access to project financial data. This promotes cooperation and the development of trust.

- Handling of Data: Financial data is promptly reported by project accounting to stakeholders so they can use it for future planning and decision-making. That way, when they need it, everyone will have access to the information they require.

- Observance: To guarantee that everything is done appropriately and compliant with the law, project accounting complies with internal policies, rules, and accounting standards. This guarantees the accuracy of the financial data and helps to prevent errors.

Project Accounting vs. Financial Accounting

While project accounting and financial accounting share similarities, they serve different purposes:

- Project Accounting: Focuses on tracking and managing the financial aspects of individual projects or initiatives.

- Financial Accounting: Focuses on reporting financial information for the entire organization, including income statements, balance sheets, and cash flow statements.

|

Aspect

|

Project Accounting

|

Financial Accounting

|

|

Focus

|

Specific to individual projects

|

Overall financial performance of the entire company

|

|

Timeframe

|

Typically short-term (project duration)

|

Long-term (usually quarterly or annually)

|

|

Purpose

|

Manage finances within a project

|

Provide a comprehensive view of company finances

|

|

Scope

|

Limited to project-related transactions

|

Encompasses all financial transactions of the company

|

|

Reporting

|

Often detailed and project-specific

|

Broad and standardized across the company

|

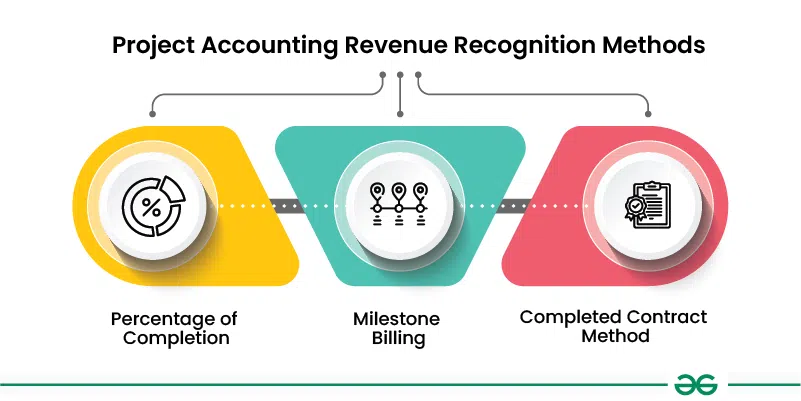

Project Accounting Revenue Recognition Methods

Common revenue recognition methods in project accounting include:

Project Accounting Revenue Recognition Methods

- Percentage of Completion: This method looks at how much of the project is done compared to the total work or costs. As the project progresses, revenue is recognized in proportion to the completion percentage. For example, if a project is 50% complete, then 50% of the total revenue is recognized.

- Milestone Billing: With this method, revenue is recognized when specific milestones or goals are reached in the project. These milestones are predetermined points in the project timeline, such as completing a certain phase or delivering a key component. Once a milestone is achieved, the corresponding revenue is recognized.

- Completed Contract Method: This method waits until the project is substantially finished or meets certain criteria outlined in the contract. Revenue is recognized only when the project is completed or reaches the agreed-upon standards. This means all revenue is recognized at once, typically at the end of the project.

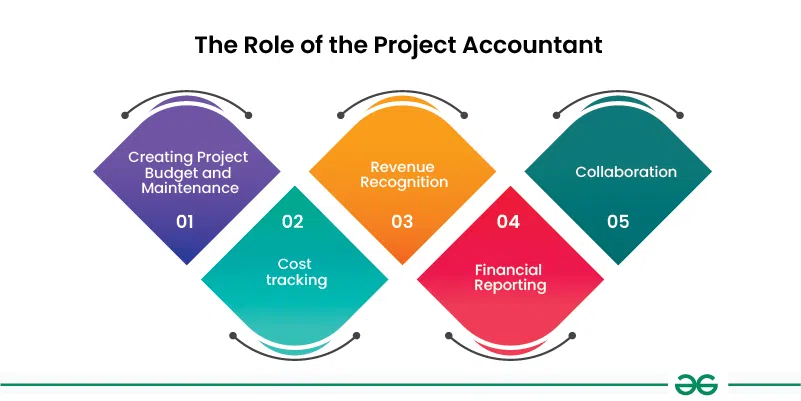

The Role of the Project Accountant

A project accountant is responsible for managing project finances, including budgeting, cost tracking, revenue recognition, and financial reporting. Their role involves collaborating with project managers, stakeholders, and finance teams to ensure projects are financially viable and meet organizational objectives.

The Role of the Project Accountant

- Creating Project Budget and Maintenance: Project budget creation and maintenance fall under the purview of the project accountant. They collaborate closely with project managers to create practical budgets that take into consideration all costs and guarantee the project’s continued financial viability.

- Cost tracking: During the course of the project, the project accountant keeps an eye on and records all project-related expenses. This involves keeping tabs on expenditures for labor, supplies, machinery, and overhead. They can spot any budgetary deviations and take necessary corrective action by closely monitoring expenses.

- Revenue Recognition: Acknowledgment of project revenue is another duty of the project accountant. This entails determining the deliverables or milestones that lead to the recognition of revenue and making sure that revenue is accurately recorded in compliance with accounting standards.

- Financial Reporting: To give stakeholders an understanding of the project’s financial performance, project accountants draft and deliver financial reports. Forecasts, variance analysis, and comparisons of the budget and actual may be included in these reports. Project managers and other stakeholders can evaluate the project’s progress toward its goals and make well-informed decisions with the aid of financial reporting.

- Collaboration: To guarantee that projects are both financially feasible and in line with organizational goals, project accountants work closely with project managers, stakeholders, and finance teams. Throughout the project lifecycle, they offer financial expertise and guidance that helps to minimize financial risks and maximize the project’s success.

Project Accounting Benefits

Project accounting offers numerous benefits, including:

- Improved Financial Visibility: Project accounting provides clear insights into how the project is performing financially. This helps project managers and stakeholders make better decisions and plan for the future with confidence, knowing exactly where the project stands financially.

- Cost Control: Project accounting helps to monitor and control project costs, ensuring that expenses stay within the budget. This prevents overspending and helps maintain financial discipline throughout the project’s lifecycle.

- Resource Optimization: Project accounting enables organizations to allocate resources—like manpower, equipment, and materials—efficiently and effectively. By optimizing resource allocation, projects can run smoothly and achieve their objectives without unnecessary waste or shortages.

- Compliance: Project accounting ensures that projects adhere to accounting standards, regulations, and internal policies. This not only fosters transparency and accountability but also mitigates the risk of non-compliance issues that could result in penalties or legal repercussions.

- Performance Evaluation: Project accounting facilitates the evaluation of project profitability, return on investment (ROI), and overall financial health. By analyzing key financial metrics, organizations can assess the success of their projects, identify areas for improvement, and make informed decisions for future endeavors.

How Project Manager Helps With Project Accounting?

Project management software like Project Manager can aid in project accounting by providing features such as:

- Budget Tracking: The software helps you monitor how much money you’ve budgeted for the project and compares it to what you’re actually spending. This way, you can see if you’re staying on track financially.

- Cost Management: This feature helps you keep tabs on all the costs involved in your project, like how much you’re spending on labor (people working on the project), materials, and other expenses. It’s like keeping a record of every penny you’re spending to make sure you’re not overspending.

- Revenue Recognition: This is about knowing when you actually earn money from the project. The software can automatically recognize when you’ve completed certain parts of the project or reached milestones, and it’ll log that as revenue earned. It’s like keeping track of when you’re getting paid for the work you’ve done.

- Reporting: Think of this as creating financial reports that show you how your project is doing financially. These reports can tell you things like whether you’re making a profit or not, where you might be spending too much money, or where you could be earning more. It’s like getting a financial check-up for your project to see how healthy it is financially.

Conclusion: Project Accounting

Project accounting is essential for tracking and managing the financial aspects of projects, ensuring they remain within budget, meet financial objectives, and comply with accounting standards and regulations. By following project accounting principles, organizations can improve financial visibility, control costs, optimize resource allocation, and make informed decisions to drive project success.

FAQs: Project Accounting

Q.1 What types of costs are typically tracked in project accounting?

Project accounting typically tracks costs such as labor, materials, equipment, subcontractor expenses, and overhead costs.

Q.2 How does revenue recognition differ in project accounting compared to financial accounting?

In project accounting, revenue recognition is often based on project progress or milestones achieved, whereas in financial accounting, revenue recognition follows generally accepted accounting principles (GAAP) and may be based on the accrual method or other specific criteria.

Q.3 What role does a project accountant play in project management?

A project accountant is responsible for managing project finances, including budgeting, cost tracking, revenue recognition, and financial reporting, to ensure projects are financially viable and meet organizational objectives.

Share your thoughts in the comments

Please Login to comment...