Difference between Internal Audit and External Audit

Last Updated :

08 Apr, 2024

Internal and External Audits contribute to organizational governance, risk management, and control processes but have distinct objectives, reporting structures, and scopes. Internal Audit is an internal function focused on improvement, while External Audit is an independent assessment primarily aimed at assuring external stakeholders.

What is Internal Audit?

Internal Audit is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps an organization achieve its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes.

Key features of internal audit include:

- Independence and Objectivity: Internal Auditors are independent of the areas they audit within the organization. This independence ensures that their assessments and recommendations are objective and unbiased.

- Systematic Approach: Internal Audit follows a systematic and structured approach to examine and assess the organization’s processes, controls, and risk management systems. This approach includes planning, conducting fieldwork, and reporting findings.

- Risk Management: Internal Audit plays a crucial role in evaluating the effectiveness of an organization’s risk management processes. It identifies potential risks and assesses whether the existing controls adequately mitigate those risks.

What is External Audit?

External Audit, also known as an Independent Audit, is a systematic examination of an organization’s financial statements, transactions, and accounting records by an external auditor. The primary purpose of an external audit is to provide an independent and objective opinion on the fairness and accuracy of the financial statements, ensuring they are presented in accordance with applicable accounting standards and regulations.

Key features of an external audit include:

- Independence: External Auditors are independent third parties who are not employees of the organization being audited. This independence is critical for ensuring objectivity and credibility in the audit process.

- Objective Opinion: The main goal of an external audit is to express an opinion on the fairness of the financial statements. The external auditor examines the evidence supporting the amounts and disclosures in the financial statements and evaluates whether they are free from material misstatements.

- Compliance with Standards: External Auditors assess whether the financial statements comply with Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS), depending on the applicable framework.

Difference between Internal Audit and External Audit

|

Basis

|

Internal Audit

|

External Audit

|

|

Meaning

|

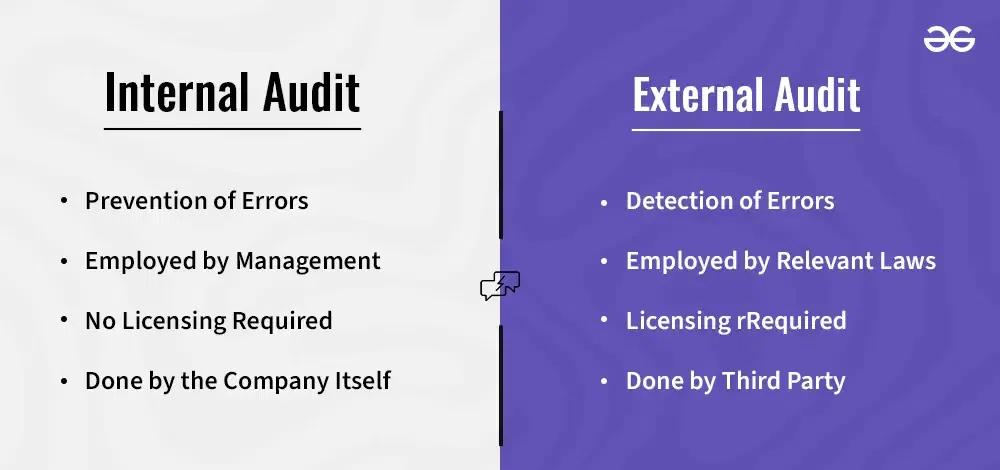

Audit which is conducted by internal auditors who are employees of the organization is known as Internal Audit.

|

Audit which is conducted by external auditors who are independent of the organization is known as External Audit.

|

|

Objective

|

The main objective is to assist management in achieving organizational objectives and enhancing operations.

|

The main objective is to provide assurance to external stakeholders, such as investors, regulators, and creditors.

|

|

Focus

|

It primarily focuses on evaluating and improving internal processes, risk management, and internal controls.

|

It primarily focuses on providing an independent and objective assessment of the financial statements and ensuring compliance with accounting standards and regulations.

|

|

Independence

|

Internal Audit may be influenced by Internal Auditors, who are employees of the organization.

|

External Audit is independent, as third parties are not affiliated with the organization.

|

|

Reporting Line

|

Reporting line is management or internal audit committee of the organization.

|

Reporting line are shareholders or board of directors of the organization.

|

|

Frequency

|

It is conducted on a regular basis, often throughout the year, as it focuses on continuous monitoring and improvement of internal processes.

|

It is usually conducted annually after the completion of the organization’s fiscal year, as it focuses on the examination of financial statements for the purpose of expressing an opinion.

|

|

Scope

|

Internal Audit is comprehensive in scope, covering various aspects of internal operations, risk management, and controls. It can include operational, compliance, and financial audits.

|

External Audit focuses specifically on the financial statements, ensuring they are presented fairly and in accordance with applicable accounting standards.

|

|

Auditor’s Relationship with Entity

|

Internal Auditor acts as a consultant and advisor to the management and internal stakeholders. They collaborates with management to enhance internal processes.

|

External Auditor maintains an independent and arm’s length relationship with the entity. They are primarily accountable to external stakeholders and regulatory authorities.

|

Internal Audit and External Audit – FAQs

Can external auditors provide consulting services to the audited organization?

Generally, external auditors are restricted from providing certain consulting services to the same organization they audit. This separation helps maintain independence and objectivity.

Can internal audit assess financial statements?

While internal audit may review financial processes and controls, its primary focus is on internal controls and risk management. The assessment of financial statements is a primary responsibility of external audit.

What areas does internal audit cover?

Internal audit can cover a broad range of areas, including financial controls, operational processes, compliance with policies and regulations, and overall organizational risk management.

Who conducts internal audits?

Internal audits are conducted by internal auditors, who are employees of the organization. They are independent from the areas they audit but are part of the internal control framework.

Who conducts external audits?

External audits are conducted by external auditors, who are independent third parties. These auditors work for audit firms separate from the organization being audited.

Share your thoughts in the comments

Please Login to comment...