Adjustment of Accrued Income in Final Accounts (Financial Statements)

Last Updated :

15 Jun, 2023

Accrued income refers to those incomes which have been earned by the firm in the current accounting period but have not been received yet. Such types of income can be Interest on loan, rent received, commission, etc. So, following the accrual concept of accounting, these incomes are recorded in the year in which they are rendered by the firm and treated as an income for the firm.

Adjustment:

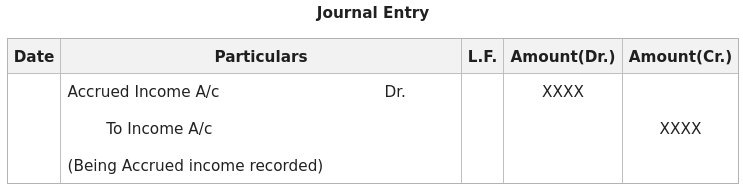

A. If Accrued Income is given outside the trial balance: In such case, two entries will be passed:

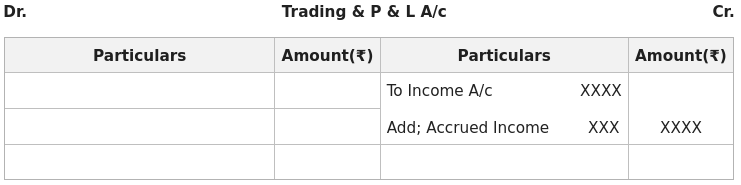

- Will be added to the related Income A/c in the Cr. side of Profit & Loss A/c.

- Will be shown in the Assets side of the Balance Sheet or added to the concerned source in the Assets side of the Balance Sheet.

B. If Accrued Income is given inside the trial balance: It will only be shown on the Assets side of the Balance Sheet.

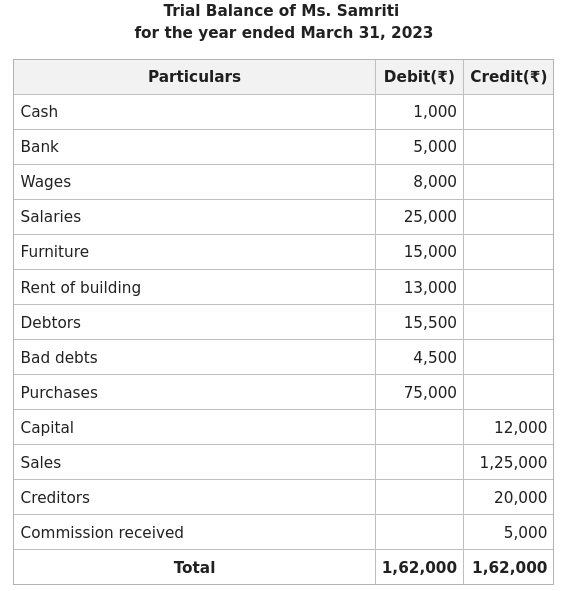

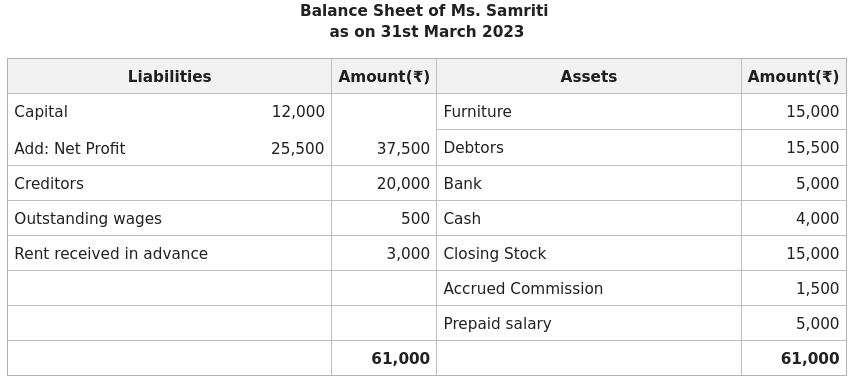

Illustration:

The Trial Balance of Ms. Samriti for the year ended March 31 2023, appears as follows:

The following adjustments were noted on that date:

1. Commission amounting to ₹1,500 is still to be received.

2. Amount of Closing stock on 31st March 2022 was ₹15,000.

3. Outstanding wages amounting to ₹500.

4. Salary paid in advance amounting to ₹5,000.

5. Rent received in advance amounts to ₹3,000.

Prepare Trading and Profit and Loss A/c and balance sheet after taking the following adjustments into consideration.

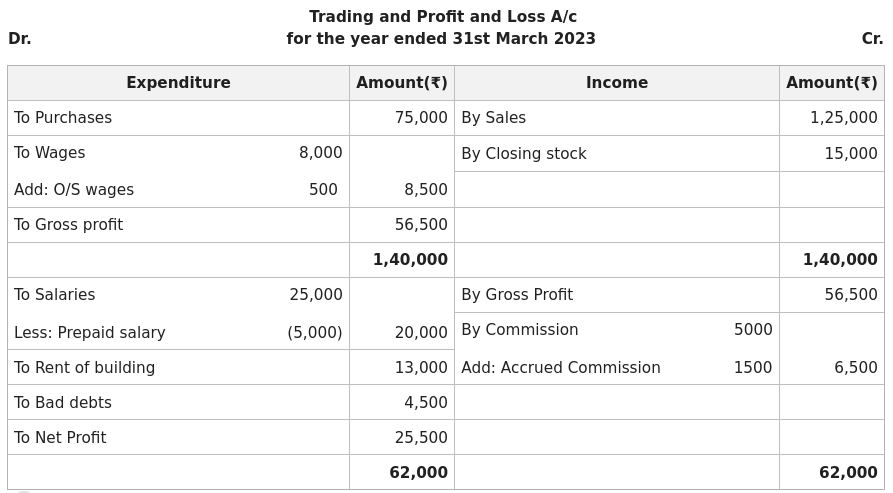

Solution:

Share your thoughts in the comments

Please Login to comment...