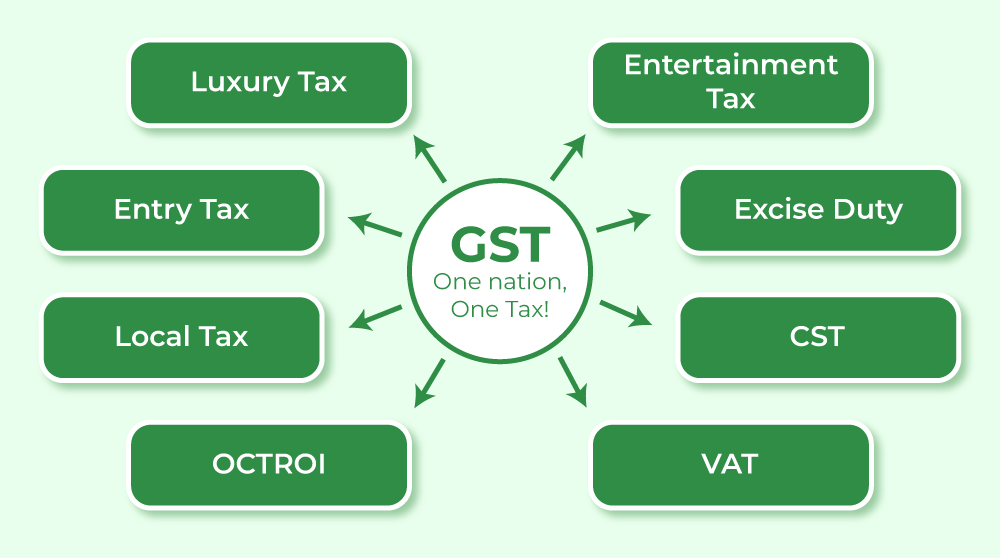

The Goods and Services Tax or GST is a single, indirect tax that integrates all indirect taxes within the Indian economy. The GST Act was passed on 29th March 2017 in the Parliament of India and came into effect on 1st July 2017. The idea behind it was to replace multiple layers of taxation with one tax (GST). It has replaced 17 indirect taxes (9 State-level taxes and 8 Central level taxes) and 23 cesses of the States and Centres that existed earlier, including Central excise duty, Service tax, Value Added Tax (VAT), Luxury Tax, etc. The aim behind implementing the GST Act was ‘One Nation and One Tax’. When GST was implemented, 1300 goods and 500 services were taken into consideration.

GST is a destination-based consumption tax as it is charged at every stage, wherever some value is added to the goods or services, and the supplier of the good or service off-sets the charge on its inputs of the previous stages. The charge is offset through the tax credit mechanism. Ultimately, the last dealer passes on the added GST to the consumer of the goods or services. The reason behind charging input credit at every stage of the value chain is to avoid the cascading effect. Cascading effect means charging tax on tax. The Government of India has eliminated the cascading effect with the expectation of reducing the prices of goods or services and benefiting the consumers.

Cascading Effect means charging tax on tax.

For example,

A company is manufacturing Good X at the cost of ₹1,000 on which it has to pay Excise Duty @ 10% to the Central Government and VAT @ 12% to the State Government.

Cost = ₹1000

Excise Duty @ 10% = ₹100

VAT @ 12% (of 1100) = ₹ 132

Therefore, the dealer’s invoice for the Good X will be ₹1,232 (1,000+100+132).

Now, the manufacturer will sell the Good to the dealer at ₹1,100.

Cost of Good X for the dealer is ₹1,100 (Cost of Good X + Excise Duty)

Suppose the dealer adds a profit margin of ₹200 on each good. Then the VAT paid by the dealer will be 12% of ₹1,300 (1,100 + 200) = ₹156.

The invoice will be ₹ 1,456 (1,100+200+156).

It can be seen that initially, Excise Duty is charged on the Good X, on which further VAT is levied. This is known as cascading effect, i.e., charging tax on tax.

GST avoids this cascading effect by charging tax only once. With GST, the tax will be charged as a percentage of the cost of goods directly.

The three types of taxes under GST are:

- Central Goods and Services Tax (CGST): GST levied by the Centre on the Intra-State supply of goods or services.

- State Goods and Services Tax (SGST): GST levied by the State (including Union Territories with legislatures) on the Intra-State supply of goods or services by the State.

- Integrated Goods and Services Tax (IGST): GST collected by the Centre and levied on the Inter-State supply of goods or services. In other terms, IGST is the total of CGST and SGST.

Facts about GST:

1. Single Tax Structure: The basic aim of GST is to replace multiple taxes with a single tax and make the price of goods or services uniform across the country. However, in doing so, some goods or services became cheaper, while some became costly.

2. Effect on Prices: Goods and Services Tax has made luxury goods costlier and goods manufactured for mass consumption cheaper.

3. Consumption-Based tax: The Goods and Services Tax is not received by the state in which the goods have been manufactured, but by the state in which the goods or services have been consumed.

4. Invoice Matching: The invoice matching mechanism will be added to the Indian GST. It means that when details of inward supply filed in by the buyer match the details of outward supplies filed in by the supplier, then only Input Tax Credit of purchased goods or services will be available to them. Besides, GST is a self-regulating mechanism, as it keeps a check on tax evasion and tax fraud and also brings more business to the formal economy.

5. Anti-Profiteering Measure: The recently implemented GST law includes the feature of anti-profiteering measures. As the name suggests, the anti-profiteering measures prevent the companies from making excess profits. According to the rules of Anti-Profiteering, the benefit of increased input tax credit and decreased GST tax rates should reach the customers in the form of a reduced price of goods or services. These provisions are efficiently managed and administered by NAA (National Anti-Profiteering Authority).

6. Registration under GST: It is mandatory for an organization with an aggregate turnover exceeding ₹ 40 Lakhs in a financial year to register under GST. However, this limit is set at ₹ 20 Lakhs for the North Eastern and hilly states (Special category states).

Input Tax Credit Under GST

Input Tax is the GST charged on the goods or services supplied to a taxable person. Input Tax Credit means reducing or adjusting the taxes paid by an individual or firm on the inputs from the taxes to be paid by them on the output, i.e., the final product. In other words, it means to claim the credit of the GST paid by an individual or a firm on the purchase of goods or services used as a raw material for manufacturing the finished goods or services. The suppliers at every stage of the supply chain have the permission to avail of any GST credit paid by them on the purchase of goods or services. This availed credit can be set off against the GST payable by them on the supply of goods or services to be made later. In this way, the ultimate consumer has to bear the GST charged by the last supplier of the supply chain. Therefore, the tax will be charged on the value added to the good or service only, which avoids the cascading effect, i.e., double taxation.

For example, if a manufacturer has paid taxes on Input A, B and C of ₹ 90, ₹ 130 and ₹ 150, respectively, and ₹ 600 on the final output, then he can claim the amount paid on input, i.e., purchase of raw material. Therefore, the manufacturer can claim (90+130+150) ₹ 370 and will have to deposit only ₹ 230 (600-370) as tax.

Key Features of GST

1. GST Rates: The States and Centres have mutually decided upon the GST rates levied on goods or services through CGST, SGST, and IGST under the aegis of the GST Council. The four tax slabs under GST are 5% (for consumer durables), 12% (general rate), 18% (general rate), and 28%(luxurious goods). However, the rate of GST for exports and supplies to the Special Economic Zones (SEZs) is 0%.

2. Applicability of GST: The Goods and Services Tax applies to the whole country (India).

3. Consumption-Based Tax: Earlier, the taxes were based on the principle of origin-based taxation. However, the Goods and Services Tax is a destination-based consumption tax, which means that the taxes will be received by the states in which the goods or services have been consumed. As the tax is received by the consumer State, the losses faced by Producer States are compensated by the Centre.

4. Applicable on Supply of Goods and Services: Earlier, the taxes were charged on the basis of ‘tax on the manufacture or sale of goods or on the provision of services; however, the Goods and Services Tax is charged on the basis of Supply of Goods and Services.

5. GST on Imports: The imports of goods and services come under IGST and is treated as Inter-State Supplies. IGST is charged on the imports of goods and services in addition to the applicable customs duties.

6. Payment of GST: The taxpayers can make payment of GST through different modes, like Internet Banking, NEFT (National Electronic Funds Transfer)/RTGS (Real Time Gross Settlement), and debit/credit cards.

Ways in which GST benefits and empowers citizens

1. Reduction in overall tax burden: It is expected that the tax burden on industries and trades will be reduced, which will result in an increase in consumption and a decrease in the price of goods and services. The ultimate result of this change is expected to be an increase in the production level and development of the industries.

2. No hidden taxes: As GST is replacing all indirect taxes with one tax, there are no chances of a hidden tax within the invoice of the goods and services. For example, if a commodity costs ₹500, it means that the overall cost of the commodity is ₹500 without any hidden taxes.

3. Development of a harmonised national market for goods and services: Harmony in tax rates, laws and procedures simplifies its compliance. The common interface of the GST portal brings synergy and efficiency to the filing of taxes. Earlier, service tax and VAT had their own returns and compliances, which was time-consuming. However, GST merges both compliances and lowers the number of returns, ultimately reducing the time spent on these compliances.

4. Higher disposable income in hand: Disposable income is the money at hand left with the consumer after making all expenses. As GST has reduced the tax burden on the taxpayers, it will increase their disposable income.

5. Customers have a wider choice: Earlier due to cascading effect, the customer used to have less disposable income at hand to spend on goods and services. But, the reduction in prices of goods and services, and tax burden has increased the disposable income of the consumers giving them a wide choice while purchasing goods and services.

6. Increased economic activity: Reduction in prices of goods and services, increase in disposable income of consumers, and decrease in the price of goods and services is leading the consumers in performing economic activities.

7. More employment opportunities: With the implementation of GST, the manufacturing of goods has become simplified, resulting in an increase in the number of manufacturers and industries. More industries will bring employment opportunities to the country, benefiting the citizens of India.

GST Council

The Goods and Service Tax Council is a constitutional body that advises the Indian Parliament. It provides recommendations to the Union and State governments about issues related to Goods and Services Tax. To provide these recommendations, it collects extensive data from the market on changes in demand for goods and services.

The Goods and Services Tax Council (GST Council) comprises:

- According to the Article 279A of the amended Constitution, the GST Council comprises the following members:

Chairperson: Finance Minister

Vice Chairperson: He/she is chosen amongst the Ministers of State Government.

Members: The members of the GST Council are MoS (Finance) and all Ministers of Finance/Taxation of every state.

- Voting takes place when at least half of the members are assembled.

- The Centre has one-third weightage, whereas the States have two-thirds of the total votes cast at the meeting.

- The decision is taken by a 75% majority.

- The Council shall make recommendations on anything related to the GST, including rules and rates, etc.

Share your thoughts in the comments

Please Login to comment...