Implementation of Lasso, Ridge and Elastic Net

Last Updated :

15 May, 2021

In this article, we will look into the implementation of different regularization techniques. First, we will start with multiple linear regression. For that, we require the python3 environment with sci-kit learn and pandas preinstall. We can also use google collaboratory or any other jupyter notebook environment.

First, we need to import some packages into our environment.

Python3

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from sklearn import datasets

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

|

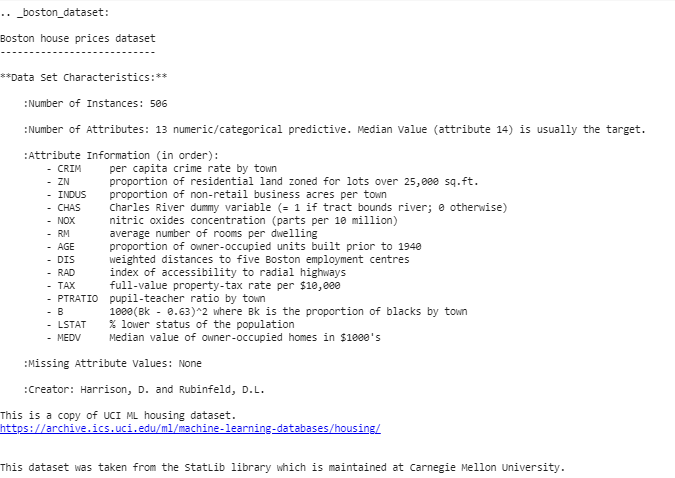

We are going to use the Boston house prediction dataset. This dataset is present in the datasets module of sklearn (scikit-learn) library. We can import this dataset as follows.

Python3

boston_dataset = datasets.load_boston()

print(boston_dataset.DESCR)

|

Output:

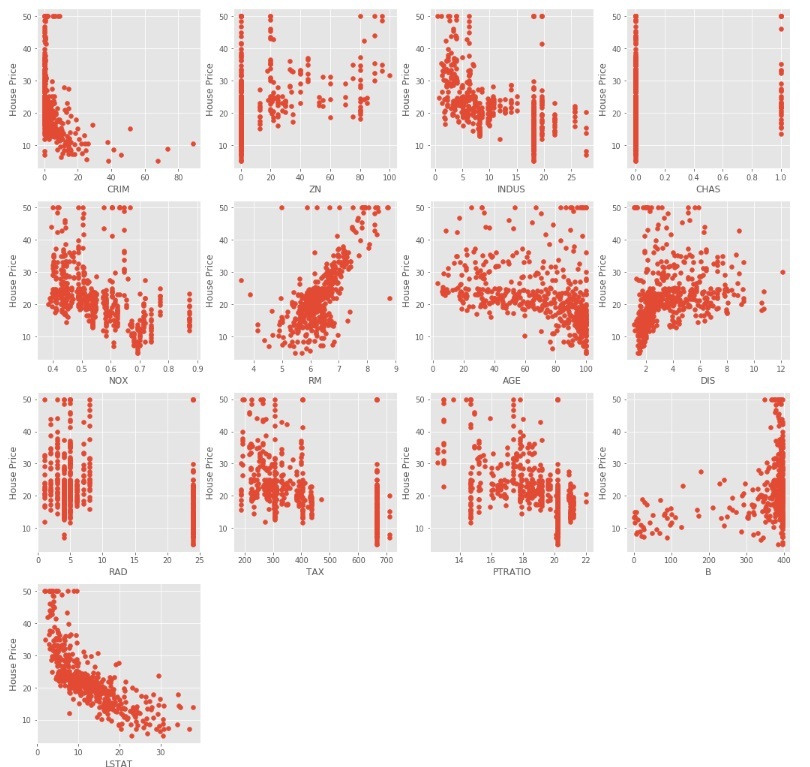

We can conclude from the above description that we have 13 independent variable and one dependent (House price) variable. Now we need to check for a correlation between independent and dependent variable. We can use scatterplot/corrplot for this.

Python3

plt.style.use('ggplot')

fig = plt.figure(figsize = (18, 18))

for index, feature_name in enumerate(boston_dataset.feature_names):

ax = fig.add_subplot(4, 4, index + 1)

ax.scatter(boston_dataset.data[:, index], boston_dataset.target)

ax.set_ylabel('House Price', size = 12)

ax.set_xlabel(feature_name, size = 12)

plt.show()

|

The above code produce scatter plots of different independent variable with target variable as shown below

We can observe from the above scatter plots that some of the independent variables are not very much correlated (either positively or negatively) with the target variable. These variables will get their coefficients to be reduced in regularization.

Code : Python code to pre-process the data.

Python3

boston_pd = pd.DataFrame(boston_dataset.data)

boston_pd.columns = boston_dataset.feature_names

boston_pd_target = np.asarray(boston_dataset.target)

boston_pd['House Price'] = pd.Series(boston_pd_target)

X = boston_pd.iloc[:, :-1]

Y = boston_pd.iloc[:, -1]

print(boston_pd.head())

|

Now, we apply train-test split to divide the dataset into two parts, one for training and another for testing. We will be using 25% of the data for testing.

Python3

x_train, x_test, y_train, y_test = train_test_split(

boston_pd.iloc[:, :-1], boston_pd.iloc[:, -1],

test_size = 0.25)

print("Train data shape of X = % s and Y = % s : "%(

x_train.shape, y_train.shape))

print("Test data shape of X = % s and Y = % s : "%(

x_test.shape, y_test.shape))

|

Multiple (Linear) Regression

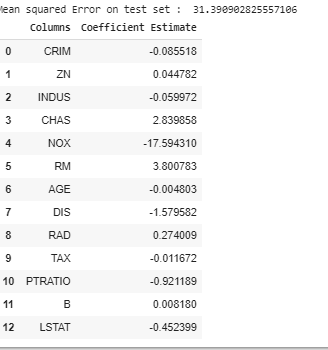

Now it’s the right time to test the models. We will be using multiple Linear Regression first. We train the model on training data and calculate the MSE on test.

Python3

lreg = LinearRegression()

lreg.fit(x_train, y_train)

lreg_y_pred = lreg.predict(x_test)

mean_squared_error = np.mean((lreg_y_pred - y_test)**2)

print("Mean squared Error on test set : ", mean_squared_error)

lreg_coefficient = pd.DataFrame()

lreg_coefficient["Columns"] = x_train.columns

lreg_coefficient['Coefficient Estimate'] = pd.Series(lreg.coef_)

print(lreg_coefficient)

|

Output:

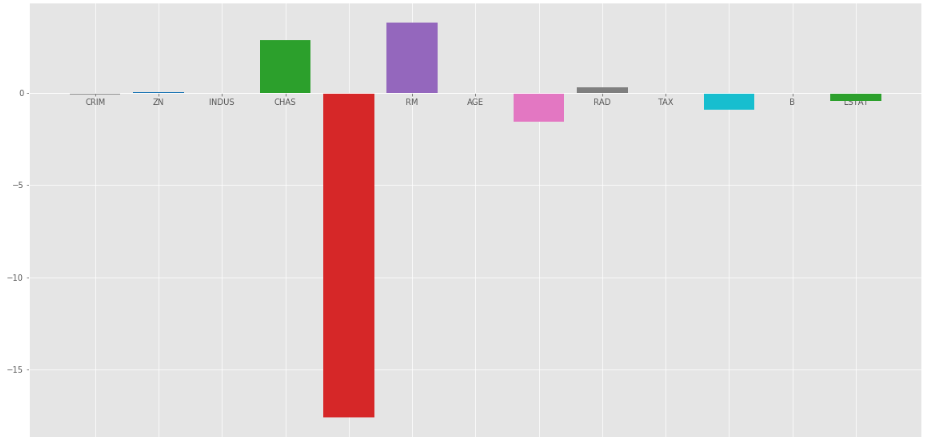

Let’s plot a bar chart of above coefficients using matplotlib plotting library.

Python3

fig, ax = plt.subplots(figsize =(20, 10))

color =['tab:gray', 'tab:blue', 'tab:orange',

'tab:green', 'tab:red', 'tab:purple', 'tab:brown',

'tab:pink', 'tab:gray', 'tab:olive', 'tab:cyan',

'tab:orange', 'tab:green', 'tab:blue', 'tab:olive']

ax.bar(lreg_coefficient["Columns"],

lreg_coefficient['Coefficient Estimate'],

color = color)

ax.spines['bottom'].set_position('zero')

plt.style.use('ggplot')

plt.show()

|

Output:

As we can observe that lots of the variables have an insignificant coefficient, these coefficients did not contribute to the model very much and need to regulate or even eliminate some of these variables.

Ridge Regression:

Ridge Regression added a term in ordinary least square error function that regularizes the value of coefficients of variables. This term is the sum of squares of coefficient multiplied by the parameter The motive of adding this term is to penalize the variable corresponding to that coefficient not very much correlated to the target variable. This term is called L2 regularization.

Code : Python code to use Ridge regression

Python3

from sklearn.linear_model import Ridge

ridgeR = Ridge(alpha = 1)

ridgeR.fit(x_train, y_train)

y_pred = ridgeR.predict(x_test)

mean_squared_error_ridge = np.mean((y_pred - y_test)**2)

print(mean_squared_error_ridge)

ridge_coefficient = pd.DataFrame()

ridge_coefficient["Columns"]= x_train.columns

ridge_coefficient['Coefficient Estimate'] = pd.Series(ridgeR.coef_)

print(ridge_coefficient)

|

Output: The value of MSE error and the dataframe with ridge coefficients.

The bar plot of above data is:

Ridge Regression at  =1

=1

In the above graph we take = 1.

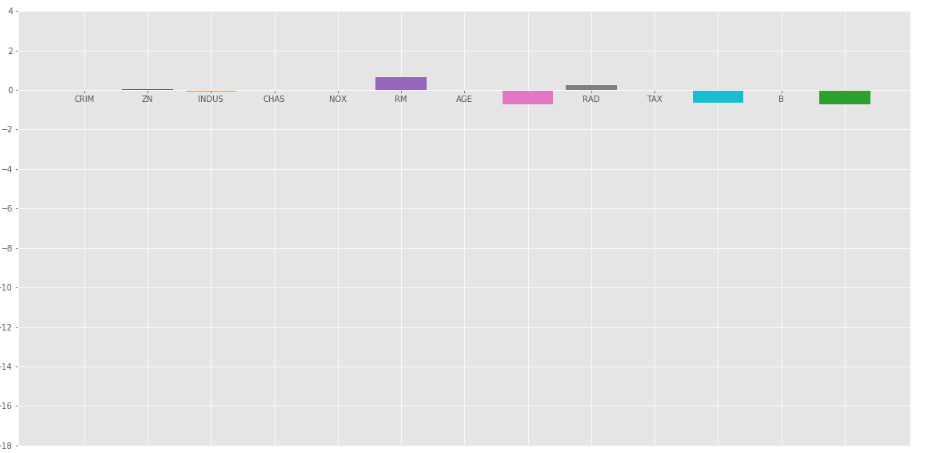

Let’s look at another bar plot with = 10

Ridge regression at = 10

As we can observe from the above plots that helps in regularizing the coefficient and make them converge faster.

Notice that the above graphs can be misleading in a way that it shows some of the coefficients become zero. In Ridge Regularization, the coefficients can never be 0, they are just too small to observe in above plots.

Lasso Regression:

Lasso Regression is similar to Ridge regression except here we add Mean Absolute value of coefficients in place of mean square value. Unlike Ridge Regression, Lasso regression can completely eliminate the variable by reducing its coefficient value to 0. The new term we added to Ordinary Least Square(OLS) is called L1 Regularization.

Code : Python code implementing the Lasso Regression

Python3

from sklearn.linear_model import Lasso

lasso = Lasso(alpha = 1)

lasso.fit(x_train, y_train)

y_pred1 = lasso.predict(x_test)

mean_squared_error = np.mean((y_pred1 - y_test)**2)

print("Mean squared error on test set", mean_squared_error)

lasso_coeff = pd.DataFrame()

lasso_coeff["Columns"] = x_train.columns

lasso_coeff['Coefficient Estimate'] = pd.Series(lasso.coef_)

print(lasso_coeff)

|

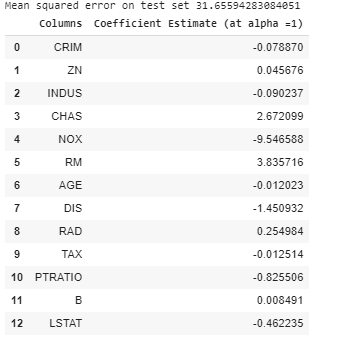

Output: The value of MSE error and the dataframe with Lasso coefficients.

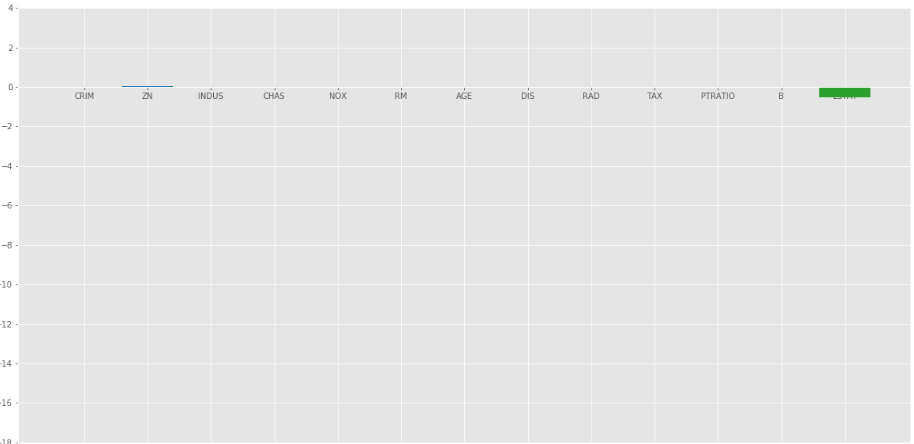

Lasso Regression with = 1

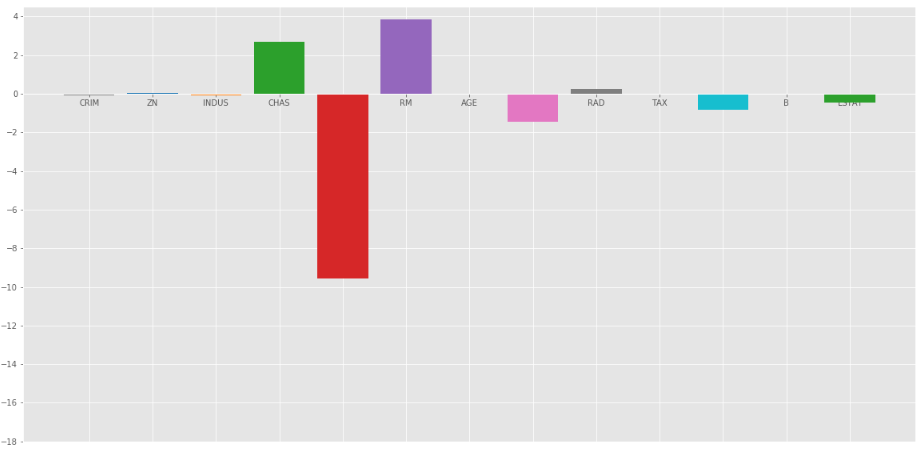

The bar plot of above coefficients:

Lasso Regression with =1

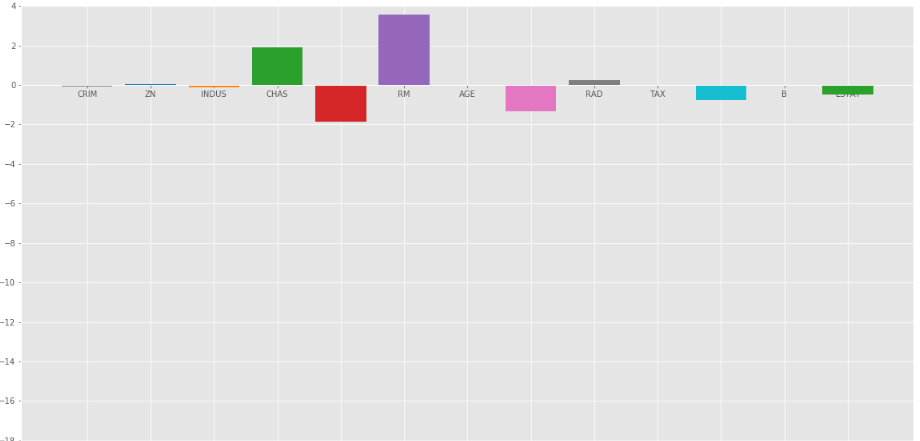

The Lasso Regression gave same result that ridge regression gave, when we increase the value of . Let’s look at another plot at = 10.

Elastic Net :

In elastic Net Regularization we added the both terms of L1 and L2 to get the final loss function. This leads us to reduce the following loss function:

where is between 0 and 1. when = 1, It reduces the penalty term to L1 penalty and if = 0, it reduces that term to L2

penalty.

Code : Python code implementing the Elastic Net

Python3

from sklearn.linear_model import ElasticNet

e_net = ElasticNet(alpha = 1)

e_net.fit(x_train, y_train)

y_pred_elastic = e_net.predict(x_test)

mean_squared_error = np.mean((y_pred_elastic - y_test)**2)

print("Mean Squared Error on test set", mean_squared_error)

e_net_coeff = pd.DataFrame()

e_net_coeff["Columns"] = x_train.columns

e_net_coeff['Coefficient Estimate'] = pd.Series(e_net.coef_)

e_net_coeff

|

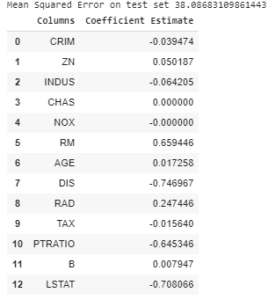

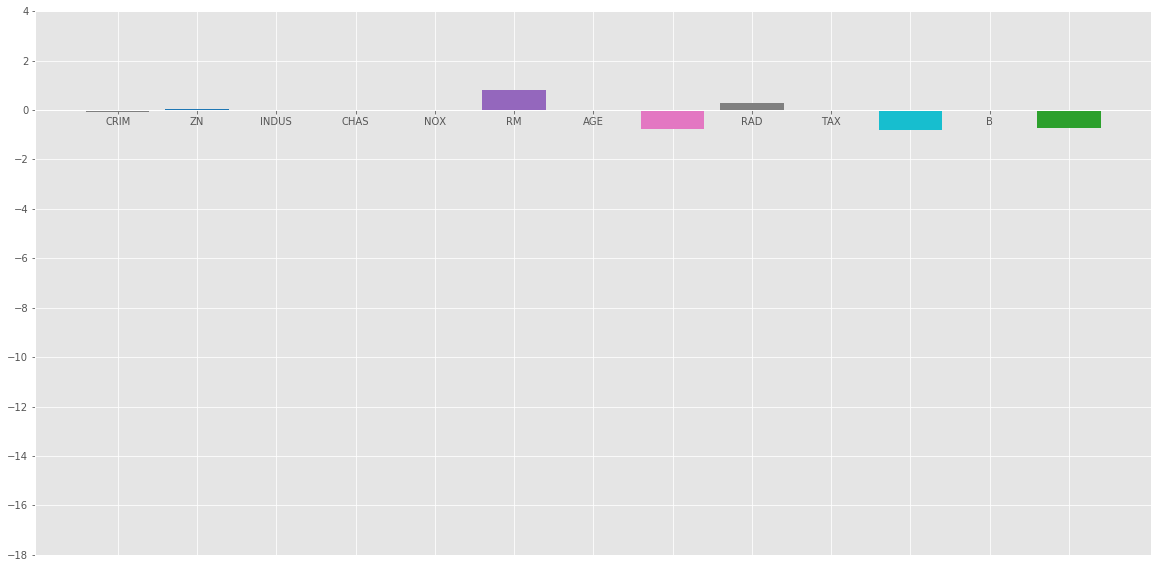

Output:

Elastic_Net

Bar plot of above coefficients:

Conclusion :

From the above analysis we can reach the following conclusion about different regularization methods:

Regularization is used to reduce the dependence on any particular independent variable by adding the penalty term to the Loss function. This term prevents the coefficients of the independent variables to take extreme values.

Ridge Regression adds L2 regularization penalty term to loss function. This term reduces the coefficients but does not make them 0 and thus doesn’t eliminate any independent variable completely. It can be used to measure the impact of the different independent variables.

Lasso Regression adds L1 regularization penalty term to loss function. This term reduces the coefficients as well as makes them 0 thus effectively eliminate the corresponding independent variable completely. It can be used for feature selection etc.

Elastic Net is a combination of both of the above regularization. It contains both the L1 and L2 as its penalty term. It performs better than Ridge and Lasso Regression for most of the test cases.

Like Article

Suggest improvement

Share your thoughts in the comments

Please Login to comment...