How to Calculate Covariance in MATLAB

Last Updated :

31 Aug, 2021

Covariance is the measure of the strength of correlation between two or more random variables. Covariance of two random variables X and Y can be defined as:

Where E(X) and E(Y) are expectation or mean of random variables X and Y respectively.

The covariance matrix of two random variables A and B is defined as

MATLAB language allows users to calculate the covariance of random variables using cov() method. Different syntax of cov() method are:

- C = cov(A)

- C = cov(A,B)

- C = cov(___,w)

- C = cov(___,nanflag)

C = cov(A)

- It returns the covariance of array A.

- If A is a scalar, then it returns 0.

- If A is a vector, then it returns the variance of vector A.

- If A is a matrix, then it considers each column as a random variable and returns the covariance matrix of matrix A.

Note: disp (x) displays the value of variable X without printing the variable name. Another way to display a variable is to type its name, which displays a leading “X =” before the value. If a variable contains an empty array, disp returns without displaying anything.

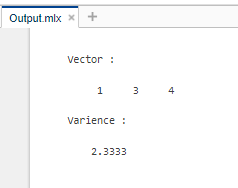

Example 1:

Matlab

A = [1 3 4];

disp("Vector :");

disp(A);

C = cov(A);

disp("Variance :");

disp(C);

|

Output :

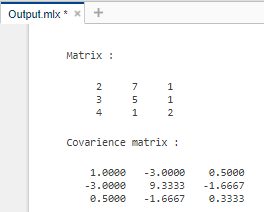

Example 2:

Matlab

A = [2 7 1;

3 5 1

4 1 2];

disp("Matrix :");

disp(A);

C = cov(A);

disp("Covariance matrix :");

disp(C);

|

Output :

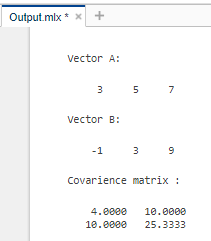

C = cov(A,B)

- It returns the covariance matrix of arrays A and B.

- If A and B vectors, then it returns the covariance matrix of A and B.

- If A and B are matrices, then it considers them as vectors themselves by expanding the dimensions and returns the covariance matrix.

Example:

Matlab

A = [3 5 7];

B = [-1 3 9];

disp("Vector A:");

disp(A);

disp("Vector B:");

disp(B);

C = cov(A,B);

disp("Covariance matrix :");

disp(C);

|

Output :

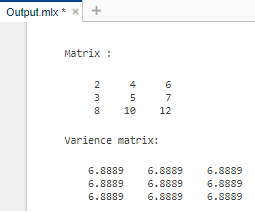

C = cov(___,w)

- It returns the covariance of the input array by normalizing it to w.

- If w = 1, then covariance is normalized by the number of rows in the input matrix.

- If w = 0, then covariance is normalized by the number of rows in the input matrix – 1.

Example:

Matlab

A = [2 4 6;

3 5 7

8 10 12];

disp("Matrix :");

disp(A);

C = cov(A,1);

disp("Variance matrix:");

disp(C);

|

Output :

C = cov(___,nanflag)

- It returns the covariance of the input array by considering the nanflag.

- If nanflag = ‘includenan’, then it considers NaN values in array.

- If nanflag = ‘omitrows’, then it omits the rows with at least one NaN value in the array.

Example:

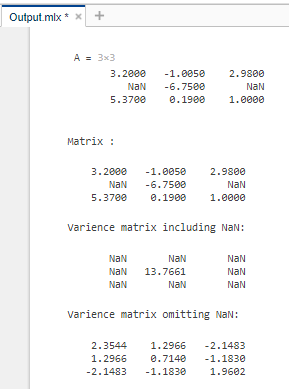

Matlab

A = [3.2 -1.005 2.98;

NaN -6.75 NaN;

5.37 0.19 1]

disp("Matrix :");

disp(A);

C = cov(A,'includenan');

disp("Variance matrix including NaN:");

disp(C);

C = cov(A,'omitrows');

disp("Variance matrix omitting NaN:");

disp(C);

|

Output :

Like Article

Suggest improvement

Share your thoughts in the comments

Please Login to comment...