What is Capital Structure?

Capital structure decisions involve determining the types of securities to be issued as well as their relative share in the capital structure. The financial decision regarding the composition of the capital structure is made after the financial requirements have been established. It entails determining how much money should be raised from each source of funding. In short, capital structure decisions involve determining the type of securities to be issued and their relative capital share.

Capital Structure refers to the proportion of debt and equity used for financial business operations.

Based on ownership, sources of business finance are classified into two categories:

- Owner’s funds(Equity): They are composed of retained earnings, preference share capital, and equity share capital.

- Borrowed funds(Debt): They are made up of bank deposits, loans, and debentures. Banks, other financial institutions, holders of debentures, and the general public may all lend money for it.

The following formula can be used to calculate the debt-to-equity ratio:

1.  ; or

; or

2.

(When debt is taken as the proportion of total capital)

Important Points about Debt and Equity:

1. Nature: Equity is the owner’s money, whereas debt represents funds that have been borrowed.

2. Cost of Debt is less than Cost of Equity: The debt involves less cost as compared to equity. First, the interest paid on the debt is deducted while calculating tax liability. Second, the risk of lenders is less than that of equity shareholders as they get assured returns every year. Thus, they require a lower rate of return as compared to equity shareholders. Hence, increasing the use of debt, while maintaining the cost of equity lowers the overall cost of capital.

3. Debt is riskier than Equity: Debt is risky because it is a legal obligation of the business to make payments of common interest. In case of failure of payment, debt holders can claim over the assets of the business and if a company doesn’t pay the return of principal, it may enter liquidation or another insolvency stage. On the other hand, equity shareholders do not create a legal obligation on the business to pay a dividend if it is running at a loss. Hence, increasing the use of debt increases the financial risk of a business.

It can be concluded that the capital structure represents the percentage of debt to equity in the capital structure. The capital structure of the business impacts the profitability and financial risk of the business. It is very difficult to define what kind of capital structure is best for a business. It must ultimately increase the value of equity shares or maximize the wealth of equity shareholders.

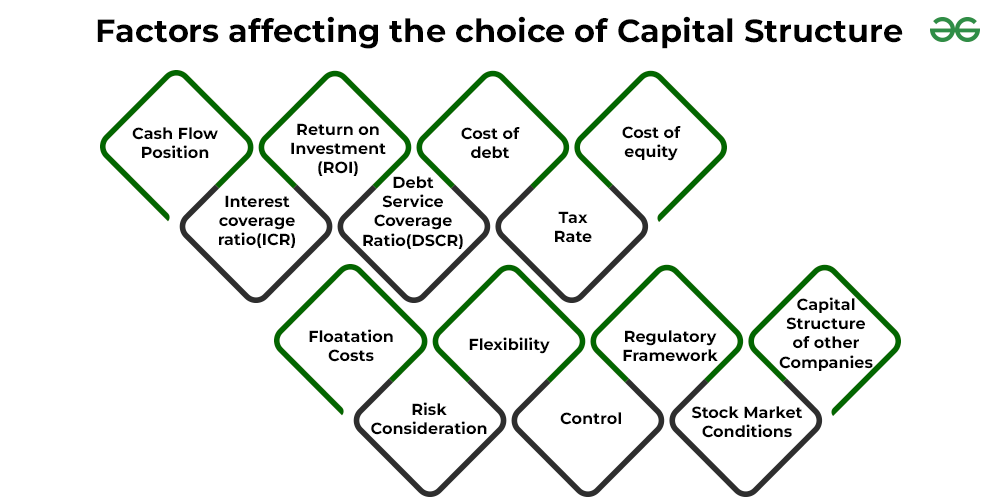

Factors affecting the Capital Structure

1. Cash Flow Position:

The composition of the capital structure is determined by the business’s ability to create cash flow. It is essential to consider the cash flow in the future to choose the capital structure. The company must have sufficient funds for funding business operations, investing in fixed assets, and fulfilling debt obligations, such as interest and capital repayments. The firm must pay dividends to preferred shareholders, fixed-rate interest to debenture holders, and loan principal and interest. Sometimes, a company produces sufficient profit but is unable to produce cash inflow for payments. If the company does not make its financial commitments, it may become insolvent. Therefore, the expected cash flow must match the obligation to make payments.

If a company is confident in its ability to generate sufficient cash flow, it should use more debt securities in its capital structure; however, if there is a cash shortage, it should use more equity securities since there is no obligation to pay its equity owners.

2. Interest coverage ratio(ICR):

ICR signifies the number of times a company’s earnings before interest taxes (EBIT) meet its interest payment. The ICR specifies the number of times EBIT can repay the interest obligation.

A high ICR shows that companies can have borrowed funds due to the lower risk of making interest payments whereas a lower ratio shows that the company should use less debt.

3. Return on Investment(ROI):

Return on Investment is a crucial factor in designing an appropriate capital structure.

In case ROI> Rate of interest, then the company must prefer borrowed funds in capital structure whereas in case ROI <Rate of interest on debt, then the company must avoid debt and use equity financing.

4. Debt Service Coverage Ratio(DSCR):

Under this, the amount of money needed to pay off debt and the capital for preferred shares is compared to the profit generated by operations.

A higher DSCR indicates a better capacity to meet cash obligations, which implies that the company can choose more debt. However, in the case of lower DSCR, the company prefers more equity.

5. Cost of debt:

The cost of debt has a direct impact on how much debt will be used in the capital structure. The company will prefer higher debt over equity if it can arrange borrowed funds at a reasonable rate of interest.

6. Tax Rate:

High tax rates reduce the cost of debt because interest paid to debt security holders is deducted from income before calculating tax, whereas businesses must pay tax on dividends paid to shareholders. So, a high tax rate implies a preference for debt, whereas a low tax rate implies a preference for equity in the capital structure.

7. Cost of equity:

The cost of equity is another aspect that influences capital structure. The usage of debt capital has an impact on the rate of return that shareholders expect from equity. The financial risk that shareholders must deal with increases as more debt is used. The required rate of return rises when the risk does as well. As a result, debt should only be used sparingly. Any use beyond the amount increases the cost of equity, and even though the EPS is higher, the share price may fall.

8. Floatation Costs:

It is the cost incurred on the issue of shares or debentures. It includes costs like advertisement, underwriting, brokerage, stamp duty, listing charges, statutory fees, etc. Before making a decision, it is important to carefully calculate the costs associated with raising money from various sources. There are additional formalities and costs associated with issuing shares and debentures. However, it is less expensive to raise funds through loans and advances.

9. Risk Consideration:

There are two categories of risk:

- Financial risk is the state in which a business is unable to pay its set financial obligations, such as interest, a dividend on preferred stock, payments to creditors, etc.

- Business risk refers to the risk of the business’s inability to pay its fixed operating expenses, such as rent, employees’ salaries, insurance premiums, etc.

Total risk refers to the sum of business and financial risk. Thus, if the company’s business risk is low, it may suffer financial risk, implying that more borrowed capital can be utilized. But when business risk is higher, debt should be used to lower financial risk.

10. Flexibility:

The firm’s ability to borrow more money may be limited by an excessive amount of debt. It must maintain some borrowing capacity to be flexible and deal with uncertain events.

11. Control:

The company’s equity stockholders are regarded as its owners, and they have complete control over it. The control of shareholders is not affected, however, by the issuance of debt. Debt should be employed if the current shareholders desire to keep control. The company might opt for equity shares if they don’t mind giving up control.

12. Regulatory Framework:

When choosing its capital structure, every company is required to follow the legal framework. The SEBI guidelines must be followed when issuing shares and debentures. Loans from banks and other financial institutions are likewise subject to several regulations. Companies may prefer to give securities as a source of additional capital if SEBI regulations are straightforward, or they may opt for more loans if monetary policies are more flexible.

13. Stock Market Conditions:

Market conditions can be divided into two categories: boom conditions and recession or depression conditions. These conditions have an impact on the capital structure, particularly if the company plans to raise further capital. Depending on the state of the market, investors might be more cautious in their dealings. People are willing to take a risk and buy stock shares even at greater prices during a boom period. Investors favour debt, which has a fixed rate of return, but, in a recession or depression period.

14. Capital Structure of other Companies:

Some businesses design their capital structures in accordance with industry norms. However, it must exercise proper care as blindly following industry standards can result in financial risk. If a company cannot afford the high risk, it should not increase debt just because other companies are doing so.

Like Article

Suggest improvement

Share your thoughts in the comments

Please Login to comment...